How Should I Invest My Money For Retirement

10 tips to aid yous heave your retirement savings — whatever your age

When planning for retirement, the truth is that the earlier you start saving, the better off you could be, thanks to the power of compound involvement. Merely even if you lot began saving belatedly or have however to brainstorm, it's important to know that you lot're not lone, and there are steps you tin have to increase your retirement savings. "Information technology'southward never besides belatedly to get started," says Debra Greenberg, director, Retirement and Personal Wealth Solutions, Bank of America.

Consider the post-obit tips, which can help you heave your savings — regardless of your current phase of life — and pursue the retirement you envision.

1. Focus on starting today

Peculiarly if yous're but beginning to put coin away for retirement, start saving as much as yous tin now and let compound interest — the ability of your avails to generate earnings, which are reinvested to generate their ain earnings — have an opportunity to work in your favor. "The earlier you can go started, the better off you'll exist," Greenberg says.

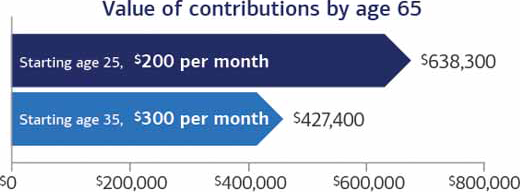

Starting early on may assist results, even investing a small amount

By starting to put abroad money earlier, a 25-twelvemonth-old investing $75 per month accumulates more assets past age 65 than if he or she had started to invest $100 per month at age 35 — despite investing less each period. Investing a smaller dollar amount over a long fourth dimension horizon tin can have a greater impact on investment results than investing a larger dollar amount for a shorter period of fourth dimension.

Investing in securities involves risks, and at that place is e'er the potential of losing coin when you invest in securities.

Source: ChartSource®, DST Systems, Inc. This example is hypothetical and does not represent the operation of a item investment. Your results will vary. Actual investing includes fees and other expenses that may result in lower returns than this hypothetical example. © 2019, DST Systems, Inc. All rights reserved. Not responsible for whatever errors or omissions.

2. Contribute to your 401(g) business relationship

If your employer offers a traditional 401(k) plan and yous're eligible, information technology may allow you lot to contribute pretax money, which can potentially exist a significant advantage. Say you're in the 12% taxation bracket and programme to contribute $100 per pay period. Since that coin comes out of your paycheck before federal income taxes are assessed, your take-home pay will driblet by only $88 (plus the amount of applicable state and local income revenue enhancement and Social Security and Medicare taxation). That means you can invest more of your income without feeling it as much in your monthly budget.Footnote 1 If your employer'due south 401(g) plan likewise offers a Roth 401(k) feature, which uses income after taxes rather than pre-tax funds, you should consider what your income revenue enhancement bracket will be in retirement to help you decide whether this is the right choice for you. Even if y'all leave that employer, y'all accept choices on what to do with your 401(k) business relationship.

iii. See your employer's match

"If your employer offers to match your 401(k) plan contributions, make sure y'all contribute at least plenty to take full advantage of the match," Greenberg says. For example, an employer may offer to match 50% of employee contributions up to v% of your salary. That means if you lot earn $fifty,000 a year and contribute $two,500 to your retirement plan, your employer would kick in another $1,250. It's essentially free money. Don't leave it on the tabular array.

4. Open an IRA

Consider establishing an individual retirement account (IRA) to help build your nest egg. You have ii options: a traditional IRA or a Roth IRA. A traditional IRA may exist right for you depending on your income and whether you or your spouse are eligible to participate in a workplace retirement plan. Contributions to a traditional IRA may be tax-deductible and the potential investment earnings have the opportunity to grow tax-deferred until you make withdrawals during retirement. If you meet the phased-out modified adjusted gross income limits, which are based on your federal tax filing condition, a Roth IRA may be a good choice for you.Footnote ii A Roth IRA is funded with later on-revenue enhancement contributions, so once you have turned age 59½, qualified distributions, including any potential earnings, are federal income taxation-free (and may be state income taxation-free) if sure belongings menstruation requirements are satisfied. To determine what type of IRA could piece of work all-time for you lot, get to Discover out which IRA may be correct for yous and view the well-nigh current 401(k) and IRA contribution limits.

5. Take advantage of take hold of-up contributions if you're age l or older

One of the reasons information technology'due south of import to starting time saving early if y'all tin can is that yearly contributions to IRAs and 401(k) plans are limited. The practiced news? As of the calendar yr you accomplish age 50, y'all're eligible to go beyond the normal limits with take hold of-up contributions to IRAs and 401(thousand)s.Footnote three So if over the years you lot haven't been able to relieve every bit much as you would've liked, catch-up contributions tin can assist heave your retirement savings.

6. Automate your savings

You've probably heard the phrase "pay yourself first." Brand your retirement contributions automatic each month and you'll have the opportunity to potentially grow your nest egg without having to think about it, Greenberg says. The Merrill Automated Funding Service (PDF) allows you to automate regular contributions to your Merrill IRA from another account at Merrill, Depository financial institution of America or other fiscal establishment. You also tin can automate your investment choice with the Merrill Automatic Investment Plan, which invests assets automatically in specific funds.Footnote four

seven. Rein in spending

Examine your budget. You might negotiate a lower rate on your auto insurance or relieve past bringing your tiffin to piece of work instead of buying it. Merrill has a cash menses reckoner that tin can help you decide where your money is going — and find places to reduce spending so you accept more to save or invest.

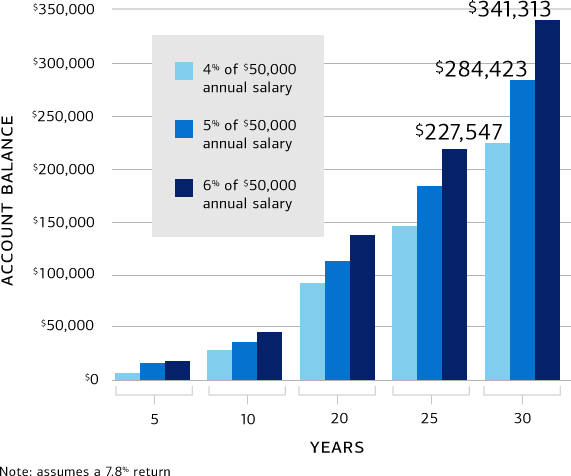

Your contribution rate: A little actress tin can help make a big departure

How much you contribute to your retirement plan business relationship today tin can make a big departure in how much you lot have when you're ready to retire. Just increasing your contribution rate from 4% to six% could add more than $101,000 to your nest egg over 30 years, assuming a $50,000 salary.

Investing in securities involves risks, and in that location is always the potential of losing money when you invest in securities.

Source: Bankrate, 401k Retirement Calculator. Instance is based on a vii.two% rate of return. This case is hypothetical and does not represent the performance of a particular investment. Your results will vary. Actual investing includes fees and other expenses that may result in lower returns than this hypothetical example.

8. Set a goal

Knowing how much you may need not only tin can help yous better empathise why you're saving, simply also can brand information technology more than rewarding. Set benchmarks along the fashion and gain satisfaction as you pursue your retirement goal. Employ the Personal Retirement Calculator to assist determine at what age you may be able to retire and how much you may need to invest and salvage to do so.

9. Stash extra funds

Extra money? Don't simply spend it. Every fourth dimension you receive a raise, increment your contribution per centum. Dedicate at least half of the new money to your retirement plan account. And while information technology may be tempting to take that tax refund or salary bonus and splurge on a new designer bag or a vacation, "don't treat those actress funds as found money," Greenberg says. She advises that you treat yourself to something modest and utilise the rest to assist make bigger leaps toward your retirement goal.

ten. Consider delaying Social Security every bit you lot get closer to retirement

"This is a big one," Greenberg says. "For every yr you can filibuster receiving a Social Security payment earlier you attain age seventy, y'all can increase the amount you receive in the future." Age 62 is the primeval you can brainstorm receiving reduced Social Security retirement benefits, but for each year you wait (until historic period 70), your monthly benefit volition increase, and the additional income adds up quickly. Pushing your retirement back even one year could make a significant departure.Footnote 5 It can also increase potential future survivor benefits for your spouse.

"Recognizing the need to put money away for retirement is the first step," Greenberg says. Understand how much you want to sock abroad for retirement and find creative means to increase your contributions. Starting too tardily and saving besides fiddling is a common regret amongst retirees. Making the try at present can help you wait forward to retirement.

Adjacent steps

- Find out if you're on runway for retirement past using our Personal Retirement Calculator to assist determine at what age you may exist able to retire and how much you lot may need to invest and save to do so

- Decide where your money is going by using our cash flow calculator

- Larn how the Merrill Retirement Evaluator can help you see where you stand up in your current retirement planning

Footnote 1 Income tax will be due upon withdrawal and you may be subject to a 10% additional federal taxation for withdrawals prior to age 59½ unless an exception applies.

Footnote two Contributions to Roth IRAs brainstorm to phase out at different modified adjusted gross income ranges for married taxpayers filing jointly, married taxpayers filing separately and singles or heads of households. Please see Roth IRA Contribution Limits for specific income amounts.

Footnote 3 http://world wide web.irs.gov/Retirement-Plans/COLA-Increases-for-Dollar-Limitations-on-Benefits-and-Contributions

Footnote 4 Please go on in mind that an automatic investment plan does not ensure a profit or protect confronting loss in declining markets. Such a plan involves continuous investment in securities regardless of fluctuating cost levels; investors should carefully consider their fiscal ability to continue their purchases through periods of fluctuating price levels.

Footnote 5 http://www.ssa.gov/retire2/delayret.html

Hypothetical functioning results accept certain inherent limitations. Hypothetical returns do not represent actual investments and are achieved through the retroactive application of investment returns with the do good of hindsight. No representation is made that a customer will achieve results similar to those shown. No representation is made that whatever account will or is likely to achieve profits or losses similar to those shown. In fact, there are frequently sharp differences between hypothetical operation results and the actual results later on achieved. The hypothetical results and functioning streams used to compile the hypothetical operation may be materially different from the customer's actual holdings.

Merrill, its affiliates, and fiscal advisors do not provide legal, revenue enhancement, or accounting advice. You should consult your legal and/or tax advisors before making any financial decisions.

MAP4263302-03092023

Source: https://www.merrilledge.com/article/10-tips-to-help-you-boost-your-retirement-savings-whatever-your-age-ose

Posted by: starkbedeencion.blogspot.com

0 Response to "How Should I Invest My Money For Retirement"

Post a Comment